How to Get Rid of PMI without Refinancing

This blog was last updated June 16, 2025.

When you’re buying a house, there are a lot of things on your mind — and private mortgage insurance (PMI) may not be one of them. PMI is often required if you have a conventional loan and make a down payment of less than 20% since your lower down payment is seen as a riskier investment for the lender. PMI isn’t designed to protect you; it’s designed to protect your lender in case you stop paying your loan. Below, we’ll cover how it works and how to drop PMI for good.

Find what you're looking for faster:

- What is Private Mortgage Insurance?

- What Does PMI Cost?

- How Much Equity Do I Need to Get Rid of PMI?

- Frequently-Asked Questions About PMI

- How to Get Rid of PMI Faster

What is Private Mortgage Insurance?

Private mortgage insurance is a mortgage surcharge that’s a common requirement for borrowers who can’t afford the down payment (which is typically 20% of the home’s purchase price), as they’re seen as a bigger risk to the lender. PMI is quite common with government-backed loans, like FHA and USDA mortgages. PMI has become more common in the past several years — in 2023, nearly 800,000 homebuyers obtained PMI.

The amount of time it takes to pay off PMI varies greatly depending on your particular situation, but a buyer who puts 10% down on a $450,000 home and pays $169 per month in PMI can expect to reach 20% equity in approximately six years.

What Does PMI Cost?

PMI is often rolled into your mortgage payment so you may not realize how much it’s costing you. With PMI costing 0.5% to 1% of an entire loan amount annually and the median listing price of a home at $427,670 as of 2024, you may be spending $356 a month on PMI.

Other PMI may require a one-time, upfront payment, and still others may require a mix of both upfront and monthly premiums. Check your loan terms if you’re unsure.

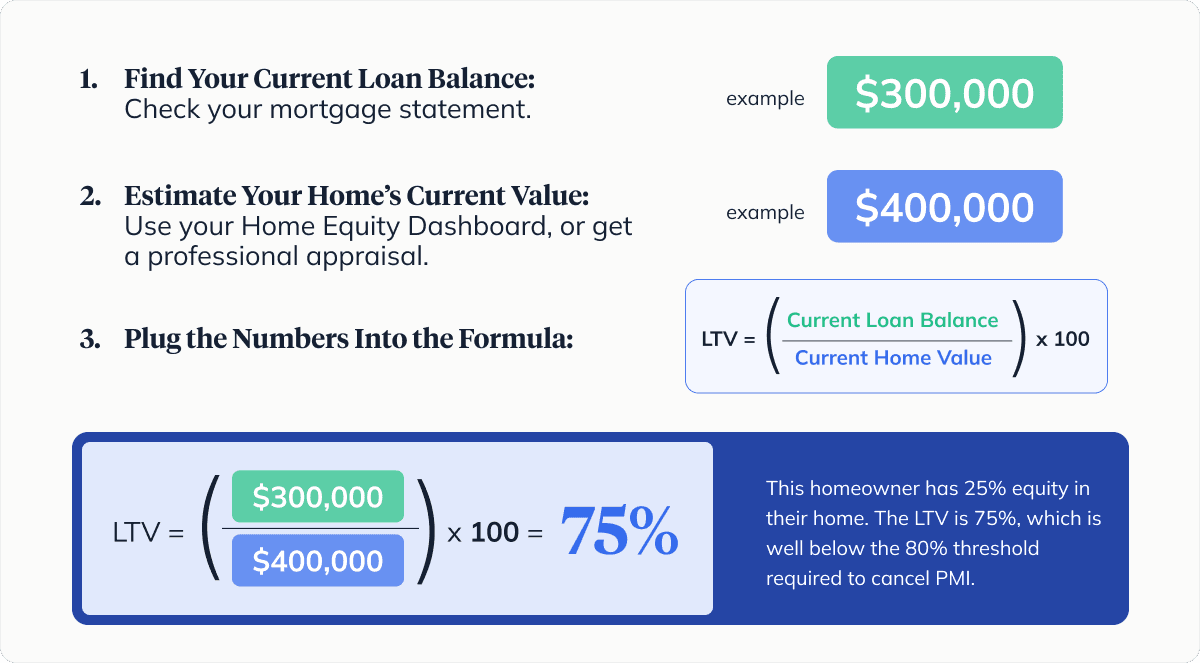

How Much Equity Do I Need to Get Rid of PMI?

If you had to get PMI when you purchased your house, then, by law, your lender had to tell you how long it would take until you no longer had to pay PMI. That’s usually when you have 20% or more equity in your home with good payment history. Some lenders require you to have a PMI contract for a certain length of time. However, it’s important to note that your lender is required to automatically terminate PMI when your loan-to-value ratio drops to 78% or your mortgage term reaches the halfway point.

How to Calculate Your PMI:

When you hit the 20% mark, you’ll want to proactively cancel PMI. Your annual statement should have information on who to call to cancel. However, this may take months as many lenders need you to put the request in writing and require a formal appraisal of the house before you can cancel. In the meantime, you still have to pay for PMI.

Frequently Asked Questions About PMI

Can I remove PMI without refinancing?

Yes, you can — there are more than a few different ways to reach the 20% equity threshold without having to refinance. These include double checking your home value through an appraisal, boosting its value with renovations, or increasing your principal mortgage payment.

Can I cancel PMI if my home value increases?

That depends on how much your home value increases. The closer to the 20% equity mark you are, the less value you’ll need to make up the difference through an updated appraisal or renovation. To avoid paying for an appraisal only to find your value hasn’t increased enough, do your homework about the ROI your renovations have added, and estimate your home value — here are some tips for predicting an accurate home value without getting an appraisal.

Do you have to pay 20% to avoid PMI?

Typically, yes. The percentage of a home’s purchase price required for a down payment varies by lender, but 20% is the typical amount necessary to bypass PMI.

How do I know if I’m still paying PMI?

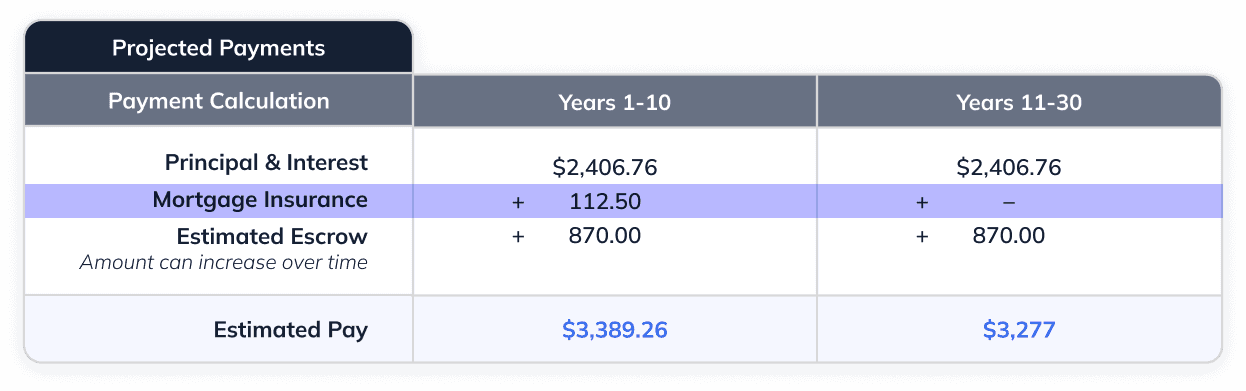

To see if you’re still paying PMI, you’ll want to look at your most recent monthly mortgage statement, as it will likely be listed as a line item in a section called “Explanation of amount due” or “Projected payments.” If you don’t see either of these on your statement, contact your lender to find out where this is documented. Here’s a sample mortgage statement. Keep in mind the location and wording can vary from lender to lender.

What is the average PMI payment?

PMI costs vary, but usually range between .5% and 6% of the total loan amount.

Is PMI tax-deductible?

No, private mortgage insurance is currently not tax-deductible — from 2018–2021, there was a PMI deduction available to homeowners that has since expired.

How is the PMI rate calculated?

The PMI rate is calculated using a variety of factors, including your loan amount, your debt-to-income ratio and credit score, and the size of your down payment. Usually, the higher your down payment, the lower your PMI rate.

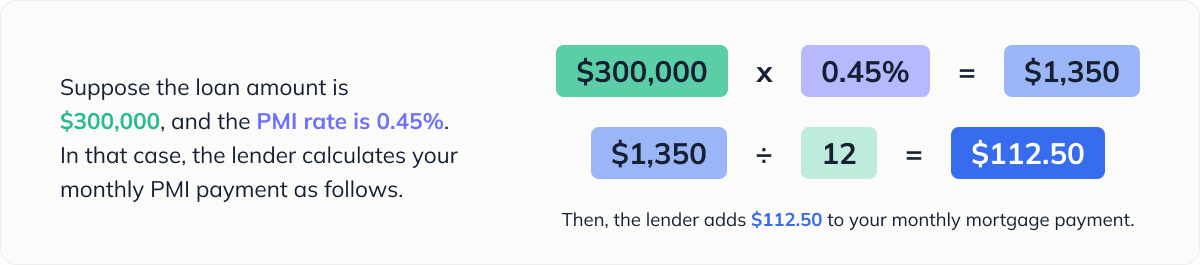

How is PMI calculated?

You can find how your monthly PMI payment is calculated by multiplying the PMI rate by the mortgage loan amount, and dividing by twelve. Here’s what that looks like, plugging in sample figures:

How to Get Rid of PMI Faster

1. Get a Home Appraisal

Before you rush to get a new appraisal, you’ll first want to check your lender’s terms. Some may require a couple of years of payments before they’ll eliminate PMI. Then, check your home value to get an up-to-date estimate — you can do this for free through your Home Equity Dashboard. If your lender has no extenuating requirements and your property value has increased, then it may be worth getting a new appraisal.

Your original home appraisal may not reflect your current standing. For example, if your home was originally appraised at $200,000 and you still owe $180,000, then you’ve paid your balance down to 90%. However, if your home has increased in value and is worth $250,000, then the outstanding balance on your mortgage is under 80% of the value of your home (you’d be at 72%, in this case). At this point, you could request cancellation.

2. Increase Your Home’s Value

Home renovations, even smaller projects, can increase your home’s value. While refinishing your basement or adding a pool could certainly increase value, think of updates like new kitchen cabinets and hardware, energy-efficient windows, a bathroom vanity, or even a fresh coat of paint. Remember: everyone’s personal style is different, so opt for more neutral tones and styles if you plan to put your home on the market in the future.

When you boost your home’s value, have your home appraised again to see if you’ve exceeded the 20% equity mark.

3. Request Early Cancellation

If your loan-to-value ratio has hit 80% or it will soon, start making your case for early cancellation. Using a mortgage amortization calculator, keep close track of where your equity stands so you can write to your lender in advance. The process can take months, so you’ll want to get it started sooner rather than later.

You’ll need three things to improve your chances for cancellation: a good payment history (no payments 30 days late in the past year or 60-day late payments in the past two years), no other liens (home equity loans or HELOCs, for example), and an appraisal, proving the home’s value.

4. Increase Your Mortgage Principal

You can make progress toward having PMI removed by increasing your monthly mortgage principal payment. If you can afford to put a bit more toward that expense, you’ll slowly but surely speed up your timeline for being PMI free.

No matter which method (or methods) you use to pay down your mortgage, you must request cancellation in writing. You’ll also want to familiarize yourself with any exceptions to PMI rules to see if any apply to your situation. Some states have laws for PMI on second homes while other rules may apply for Federal Housing Administration or Department of Veterans Affairs loans. Gather all the facts as they relate to your specific home loan and financial situation to determine which method makes the most sense to eliminate your PMI.

From a renovation calculator to help estimate ROI to a home value estimate you can trust — and track over time — our free Home Equity Dashboard is a tool every homeowner should know about. Create your account in just minutes.

You should know

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

Related Tags:

Home appraisal