Designing Home Equity Products for How Life Actually Happens

It's easy to get lost in the spreadsheet.

As someone who spends her days analyzing home equity product structures, pricing models, and investment scenarios, I think about financial products in terms of dollars and cents — running asset cash flow models, stress-testing structural parameters, optimizing for product-market fit. But here's what I've learned: while we're focused on expected cost of capital and return projections, homeowners are asking themselves entirely different questions.

Questions like: Is this additional monthly payment at the “grocery bill” level, or are we talking “car payment” territory? How much stress does this add to my life? Can I still afford this if my circumstances change?

Our recent survey of 1,000 U.S. homeowners revealed a striking disconnect between how the industry thinks about home equity financing and how homeowners actually experience it. Homeowners aren't poring over amortization tables or parsing basis points; they're navigating a mix of emotional psychology, mental accounting, and real-time risk assessment, usually under circumstances that didn't announce themselves in advance. That gap isn't just about products. It's about a fundamental difference in perspective, and it's costing both homeowners and lenders.

The Human Math Behind Financial Decisions

When homeowners tap into their equity, they're rarely doing so because their spreadsheets told them the moment was right. They're doing it because life happened.

Someone lost their job. A parent needs care. A child is heading to college. The HVAC failed. The family is growing, or changing, or relocating.

According to our survey, 65% of homeowners are most concerned with covering unexpected home costs — not maximizing their investment returns or optimizing their debt structure. They need responsive financial tools that match their reality: life doesn't follow the neat timeline of a fixed term length or a fixed monthly payment schedule.

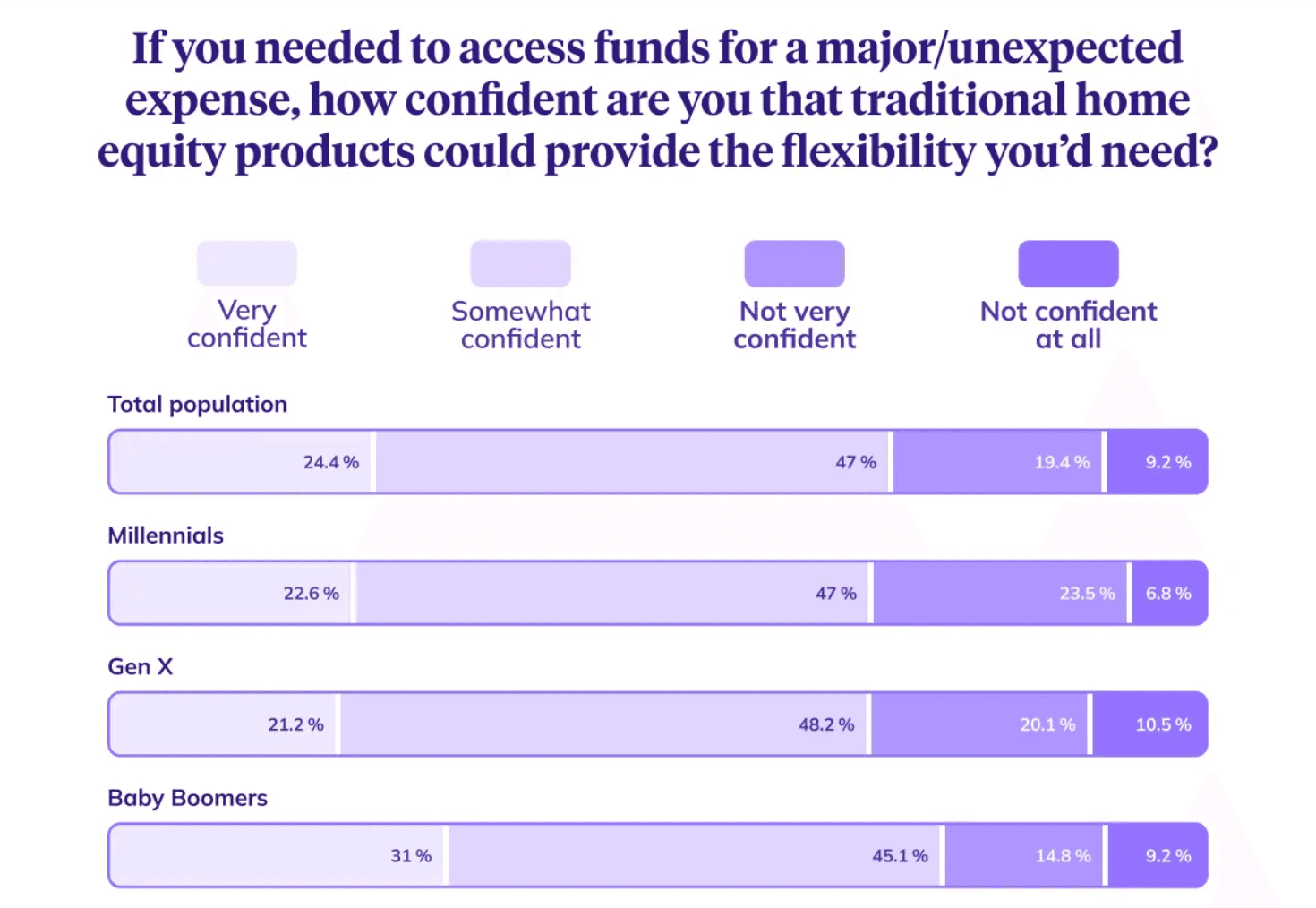

Younger homeowners feel this especially acutely. Our data shows that millennials and Gen X show markedly less confidence in traditional products than baby boomers, and express a stronger appetite for flexible alternatives. As one analysis of consumer demand for innovative mortgage solutions points out, younger generations entering the housing market have distinct financial behaviors and priorities, often preferring transparency and flexibility over traditional product features.

In other words, the math that matters to homeowners isn't about rate arbitrage but rather what they can support in their monthly budget while maintaining their quality of life. Every additional fixed monthly payment makes them less nimble, and most of the questions homeowners ask themselves boil down to one central theme: the loss of freedom. They’re weighing the current utility of accessing equity against their future flexibility. If we design products solely around risk models and loan performance metrics, we risk losing sight of the actual people using them.

The Trust Deficit

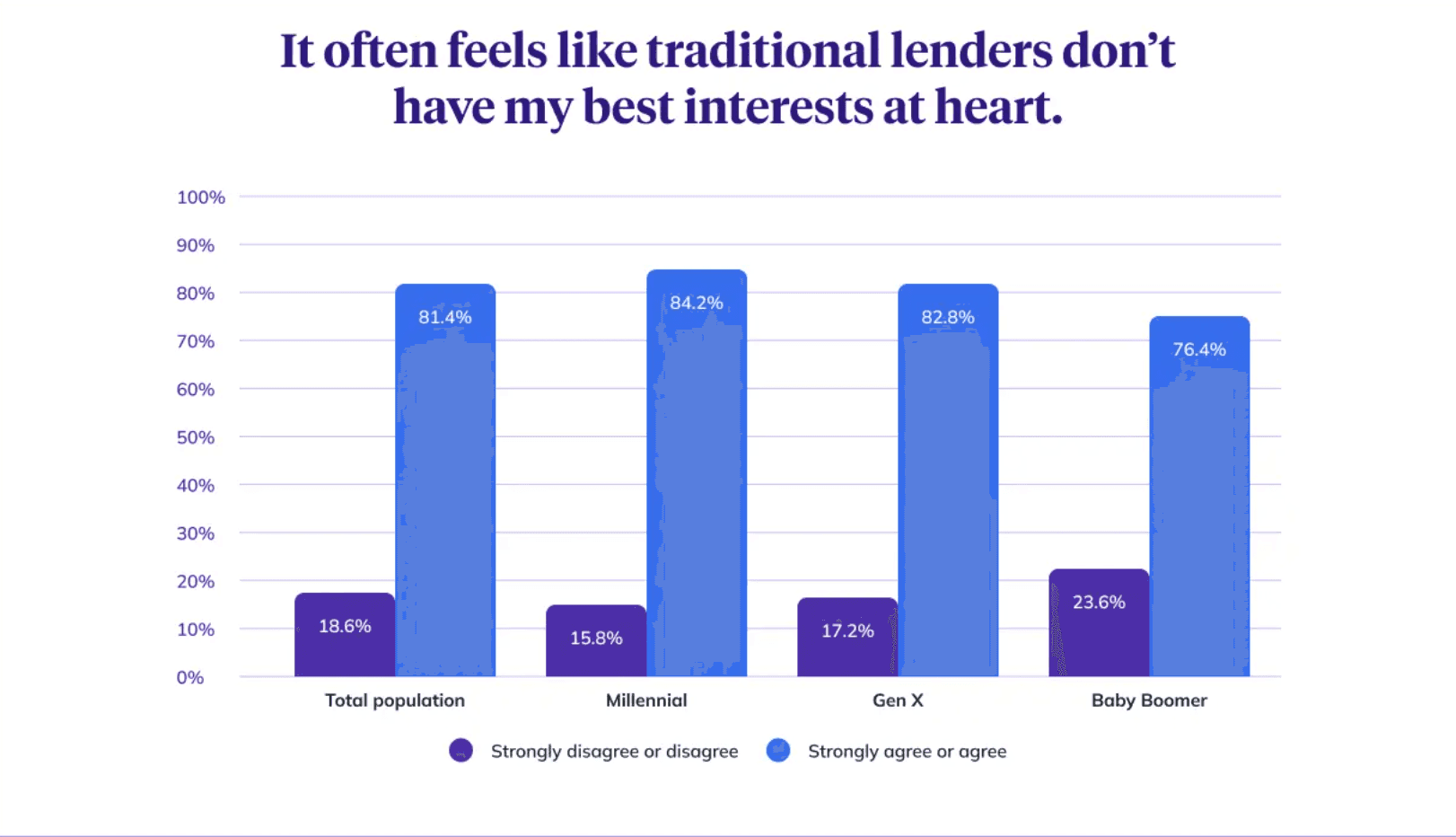

Perhaps the most sobering finding in our research: 81% of homeowners agree that traditional lenders don't have their best interests at heart.

That's not a PR problem. It's a credibility crisis, and it’s not hard to understand why.

Financial decisions happen during vulnerable moments. When you're worried about paying for your daughter's tuition, or your father needs to move into assisted living, or the foundation is cracking and you can’t wait six months for loan approval, the last thing you want is to suspect the person across the table is optimizing for their quarterly numbers rather than your situation. Without trust and credibility, homeowners may delay decisions, make less-than-ideal choices, or avoid traditional products altogether — especially when you consider the financial commitment today’s options require.

That distrust has real consequences. According to our survey results, 20% of respondents have avoided traditional home equity products entirely due to rising rates and costs; another 11% have delayed using them. When homeowners need major funding, only 8% would choose a HELOC first, and just 5% a home equity loan. When the need is real and the products exist, yet homeowners still aren't reaching for them, that's worth paying attention to.

What Homeowners Actually Want

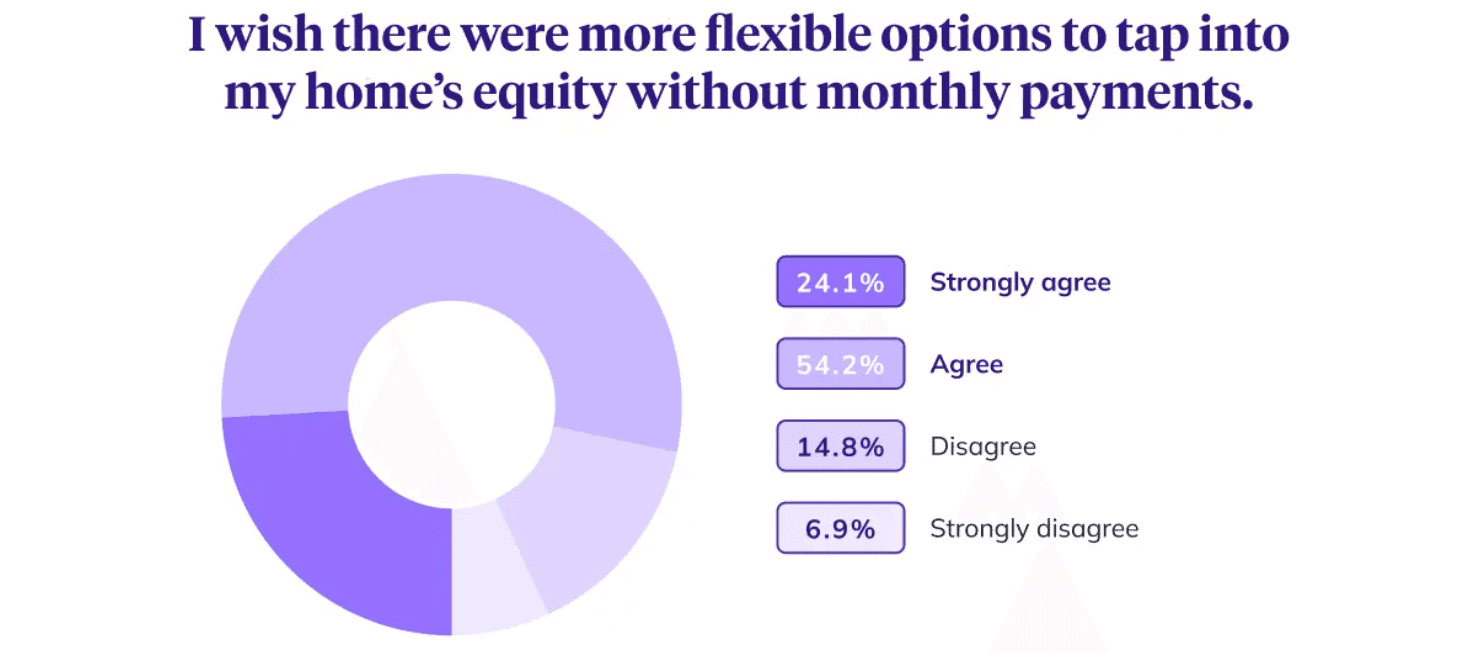

When we asked homeowners what matters most when choosing a financing product, 39% prioritized lower fees and closing costs — they want the process to be accessible. 78% wish there were more flexible options to tap into their home's equity without monthly payments, with “flexible” meaning everything from adjustable terms to the ability to pause payments when circumstances change.

These aren't radical requests. Homeowners are asking for financial products that acknowledge real life: uncertainty, shifting income, competing priorities. They're asking for partners, not just products.

But flexibility isn’t free, and the most useful thing the industry can do is be honest about that.

The Real Tradeoffs

Home equity investments (HEIs), for example, allow homeowners to access their equity without monthly payments. Instead, the homeowner shares a portion of their home's future value with the investor. If home prices rise significantly, there’s an annual IRR cap to protect the homeowner, but this could still mean giving up more long-term value than a traditional debt product would have cost.

That's a real tradeoff. Peace of mind in the near term could come at the expense of potential future upside. An HEI isn’t the right fit for every homeowner, and that's the point.

For homeowners with stable income who can comfortably carry a monthly payment and want to retain full upside on their home's appreciation, traditional products often make good sense — that's exactly who they were designed for. But there's a meaningful subset of homeowners for whom that monthly payment adds genuine stress: people managing income volatility, navigating a job transition, or prioritizing cash flow for other pressing needs. For them, trading some future appreciation for near-term stability isn't just rational; it's valuable. And then there are homeowners who qualify for traditional products on paper but simply prefer the flexibility an HEI provides. That preference is legitimate too.

The problem has never been that traditional products exist. It's that the industry has too often treated them as the right fit for every homeowner's circumstances.

Innovation as Business Imperative

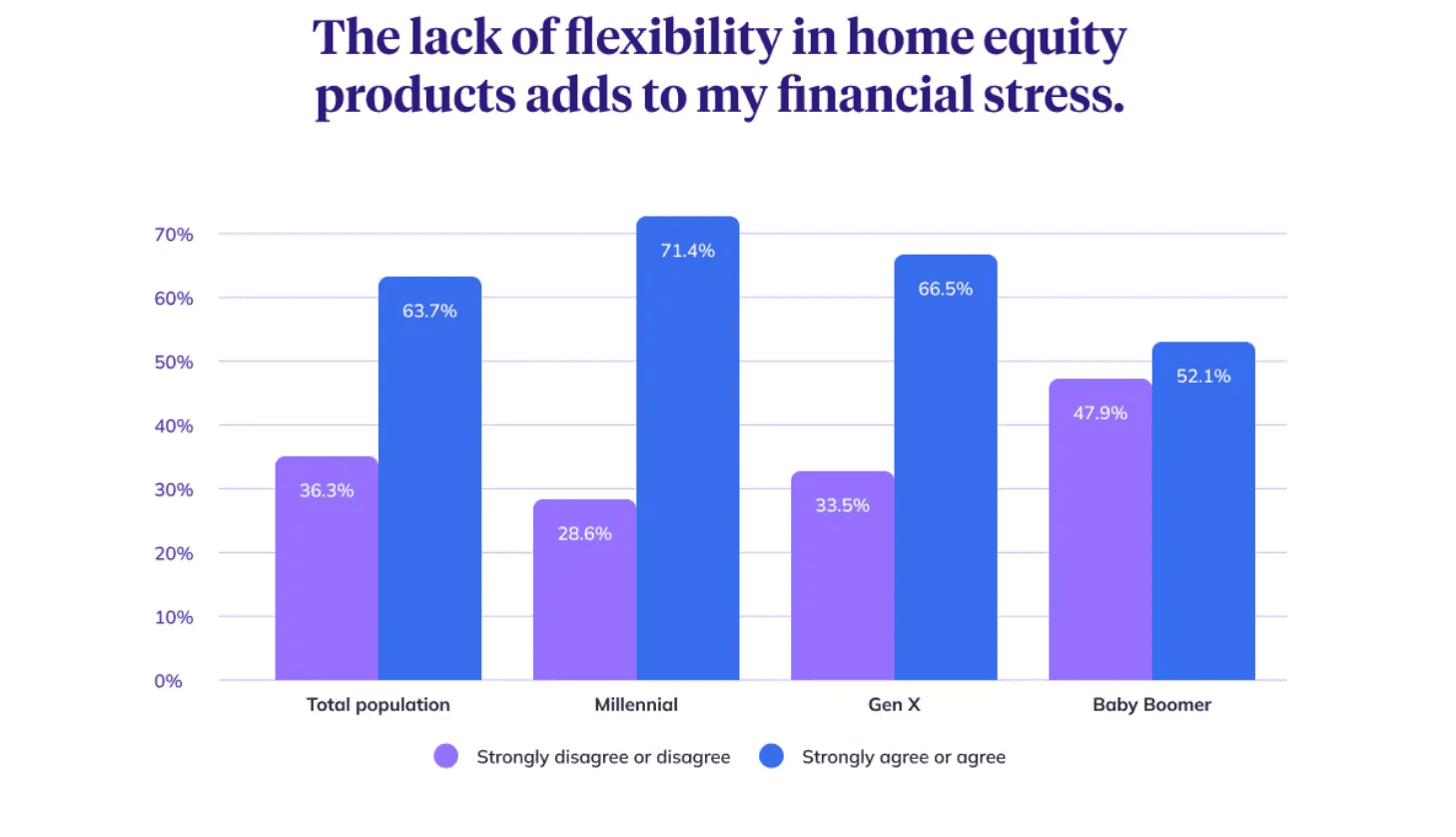

Our survey found that 72% find the traditional process outdated and difficult, and 64% say the lack of flexibility adds to their financial stress. These aren't minor pain points but rather market signals.

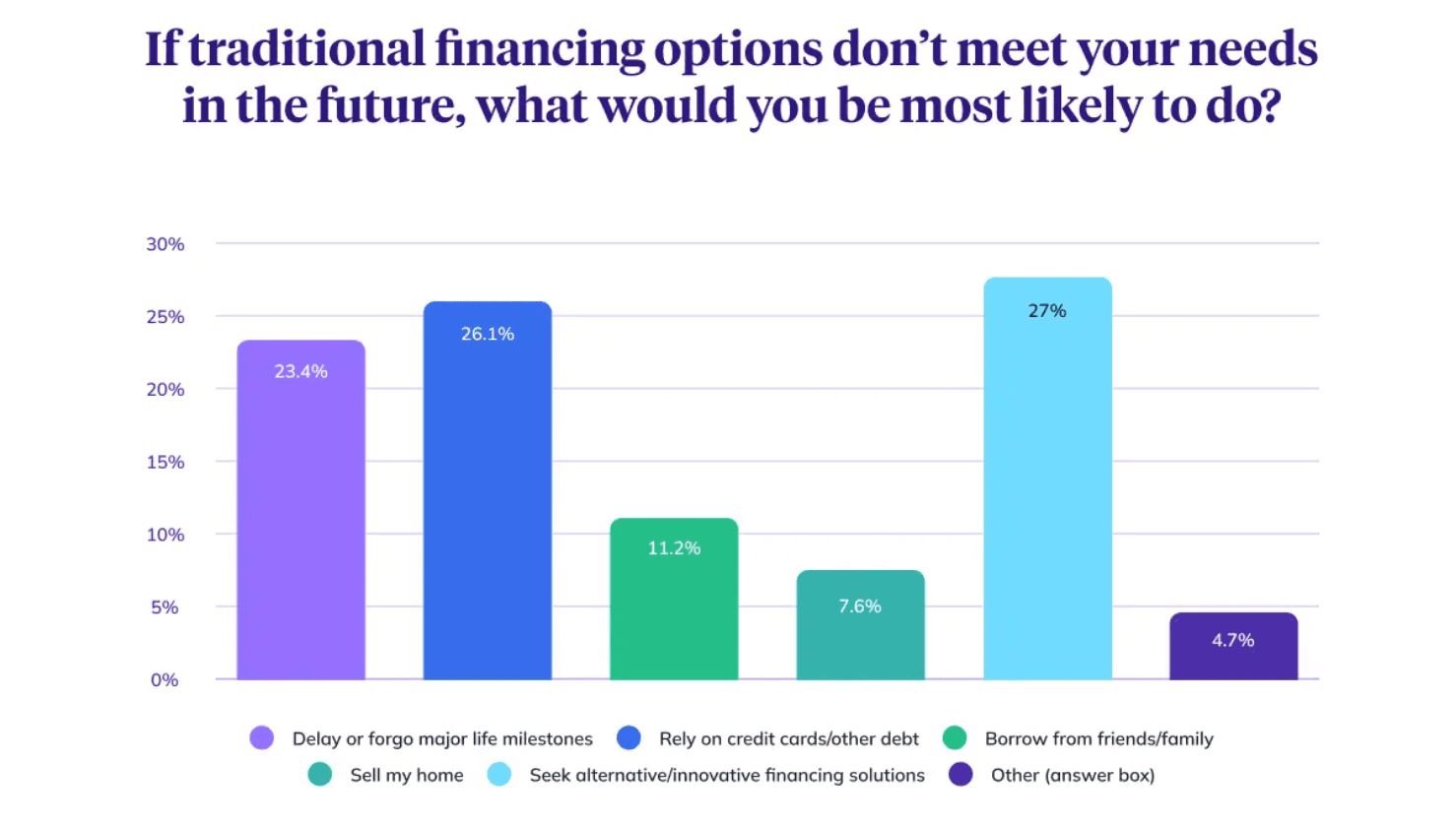

Meanwhile, more than a quarter of homeowners said that if traditional options don't meet their needs, they'll seek alternative or innovative financing solutions. Among millennials specifically, 71% say lack of flexibility adds to their financial stress (compared to 52% of baby boomers). Nearly four out of five millennials want more flexible options without monthly payments (compared to 70% of boomers), and 84% feel traditional lenders don't have their best interests at heart.

This is the generation that will shape the housing market for the next three decades. If the industry doesn't innovate to meet their needs, they'll find (or create) alternatives. The companies that design for how humans actually live, that start with life events and work backward to product design, won't just serve homeowners better. They'll capture market share from institutions who are still optimizing for impersonal aspects that homeowners don’t care about.

From Products to Partnerships

So what does this mean in practice?

It means transparency: Not burying the true cost of products in fine print. As the industry analysis notes, lenders play a crucial role in educating consumers about available options and empowering them to choose what fits their needs. Transparent communication builds trust and strengthens long-term customer relationships in a way that good rates alone can't.

It means flexibility: Creating products that can adapt when life changes, rather than locking homeowners into rigid terms that might have made sense at signing but not in year three.

And it means alignment: Structuring products that deliver strong value-propositions for both the homeowner and the financer.

The data is clear: 75% of homeowners believe the industry needs new types of financing options beyond traditional mortgages, HELOCs, and home equity loans. They're not asking us to abandon underwriting standards or throw risk management out the window. They're asking us to start at the kitchen table and work backward to the spreadsheet.

When I'm running pricing models and stress-testing product structures, I'm looking at a spreadsheet version of reality that’s clean, quantifiable, and controllable. But when a homeowner is sitting at their kitchen table trying to figure out how to pay for their kid's college while keeping the roof from caving in, they're living in an entirely different reality.

Our job isn't to force homeowners into our spreadsheets. It's to design and build products that actually work in their day-to-day lives.

You should know

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

Related Tags:

Home equityMore in “Market insights”

Urban Institute’s “How Shared Equity Products Work, Who Is Using Them, and Regulatory Recommendations” Report — and Why it Matters for the Industry

The True Cost of Homeownership in Florida: What to Expect