Urban Institute’s “How Shared Equity Products Work, Who Is Using Them, and Regulatory Recommendations” Report — and Why it Matters for the Industry

The Urban Institute, one of the nation's most respected independent housing policy research organizations, recently published the most comprehensive study of the home equity investment industry to date.

Authored by Urban Institute Housing Finance Policy Center founder Laurie Goodman and research analyst Katie Visalli, the report analyzes data from approximately 54,000 home equity investments, also referred to as shared equity agreements, originated between 2015 and 2025 by the Coalition for Home Equity Partnership (CHEP)’s three founding members: Hometap Equity Partners, LLC, Point Digital Finance, Inc. and Unlock Technologies, Inc. The report comprehensively examines:

- Who uses home equity investments (HEIs)

- Why they use them

- How the products are structured

- How they differ from traditional mortgage loans, and

- What an appropriate regulatory framework should look like

The findings are entirely independent. CHEP members provided data but had no influence over the conclusions. This is a data-driven analysis of facts, not a subjective assessment of the industry.

Key Findings & Insights

Home equity investments are filling a critical gap in the market.

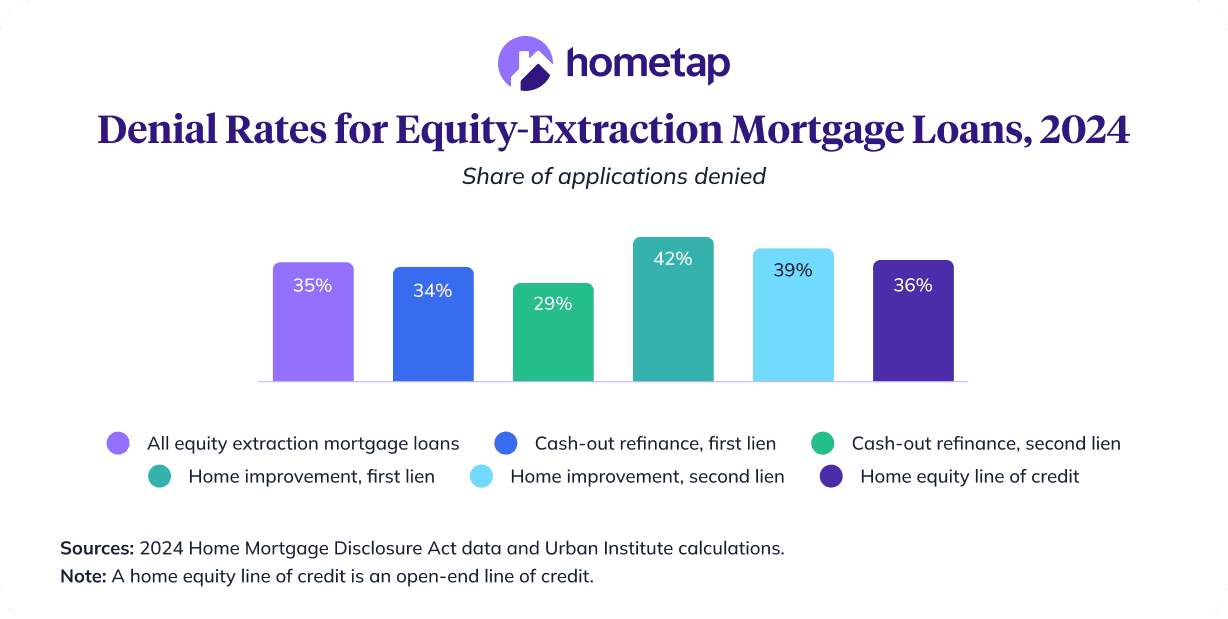

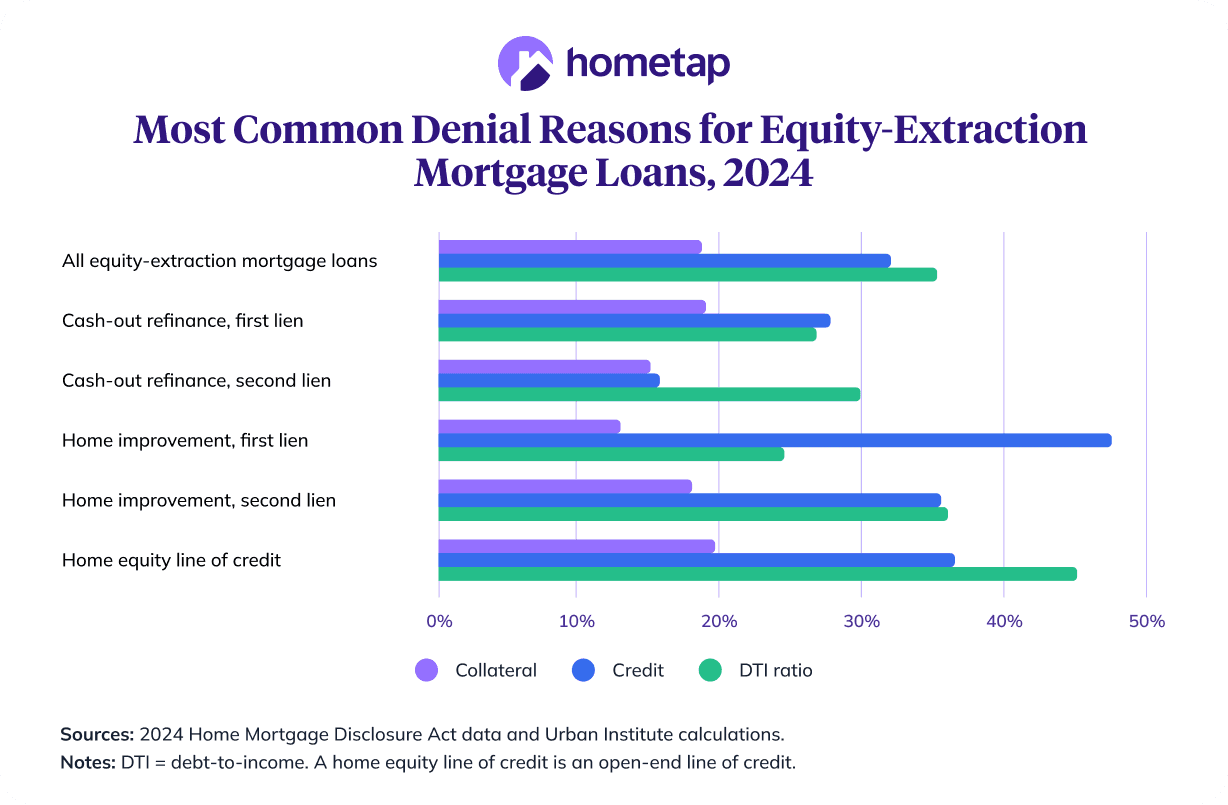

More than a third of homeowners who apply for a traditional equity extraction mortgage are denied.

More than 80% of outstanding mortgage loans have interest rates below 6%, meaning many homeowners are unwilling to give up their low rates for a cash-out refinance. This makes HEIs an even more attractive alternative. HEIs also serve as an appealing option for homeowners who either can’t qualify for a traditional mortgage loan — or who simply do not want the burden of an additional monthly payment — but want to put the wealth stored in their home to work.

HEIs serve a broad range of homeowners.

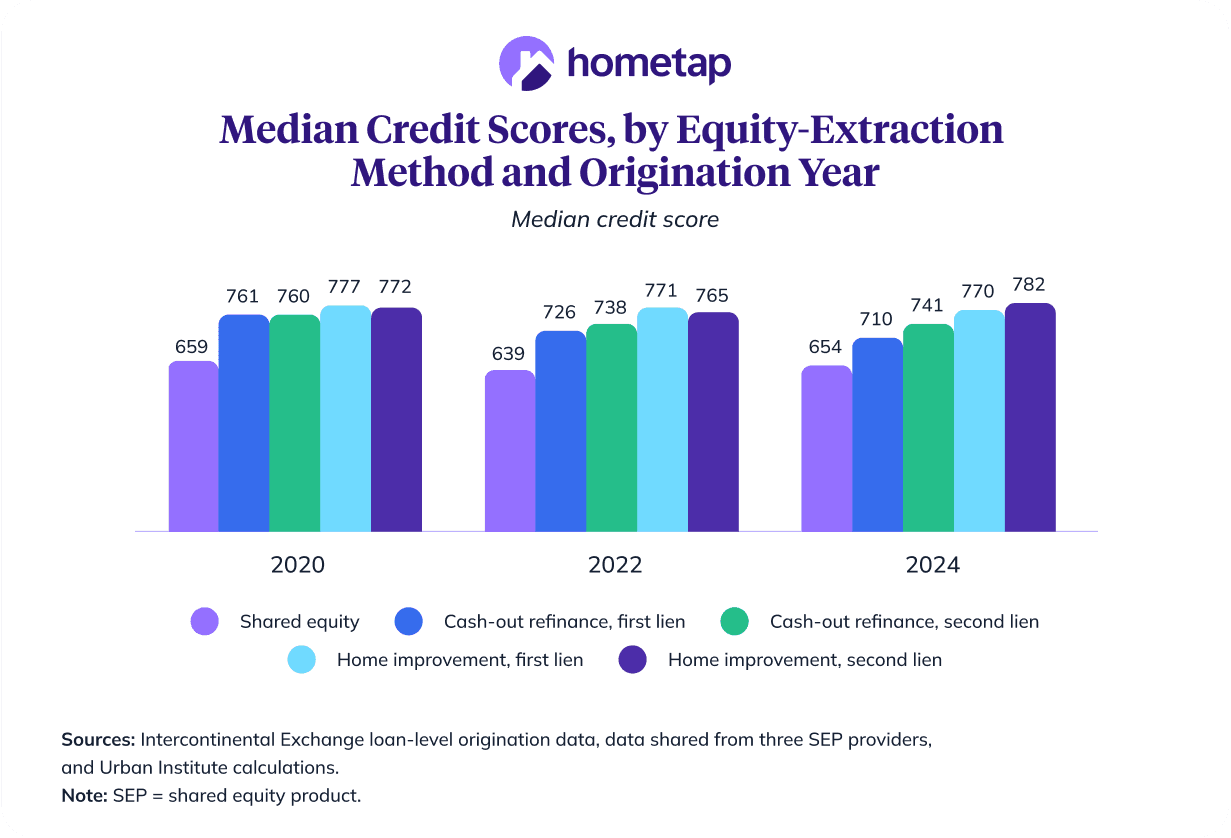

The research confirms that homeowners with HEIs closely mirror traditional mortgage borrowers in age, income, and amount of equity extracted. In other words, this isn’t a niche product serving a niche audience.

Homeowners are using HEIs responsibly.

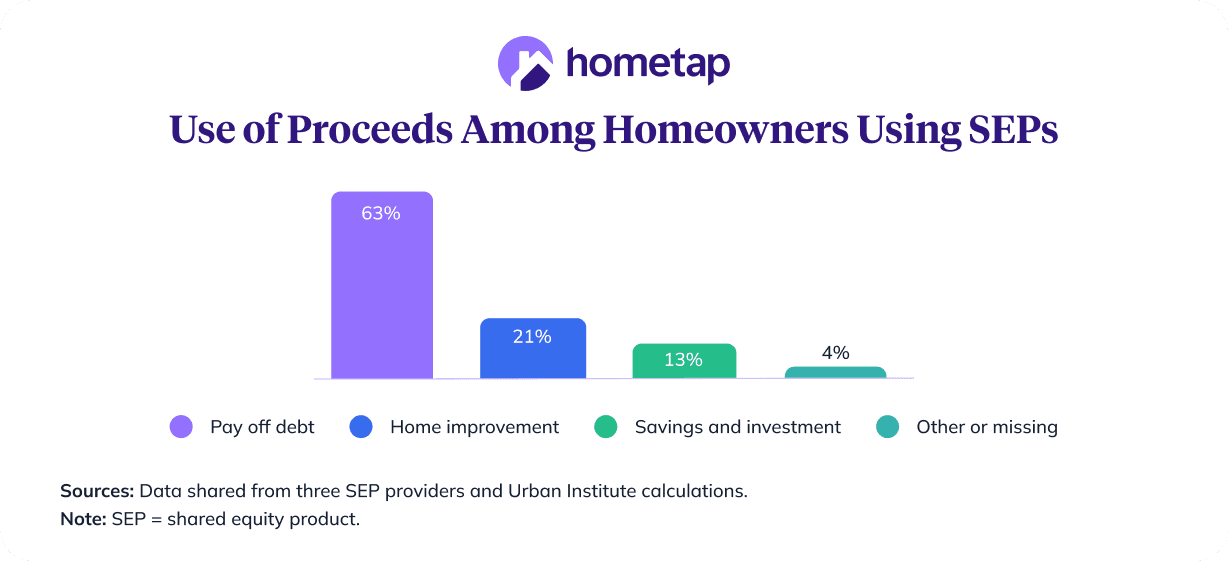

The cash homeowners receive from home equity investments is decidedly spent with purpose. 63% of homeowners are using proceeds to pay down debt and 21% using them for home improvement. These are goal-oriented financial decisions made by homeowners looking to improve their long-term financial position.

What’s next? A tailored regulatory framework is on the horizon.

The report calls for a regulatory framework designed specifically for home equity investments, not adapted from mortgage lending rules. This would strengthen consumer protections, reduce regulatory uncertainty — and ultimately lower costs for homeowners.

You should know

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

More in “Market insights”

Survey: Why Meeting Small Business Owners Where They are Matters in 2026

The True Cost of Homeownership in Florida: What to Expect