Fund Your Child's Tuition without Touching Your Retirement Savings

As the cost of higher education skyrockets, many parents are understandably concerned about how they may be able to cover tuition and fees without using retirement funds to pay for college. A recent report found that 68% of parents would consider pulling from their retirement savings to help pay for their children’s college education. At the same time, 41% of Americans don’t think they’ll have enough money saved to retire, creating a precarious situation for families who are trying to handle day-to-day costs on top of pursuing long-term financial goals.

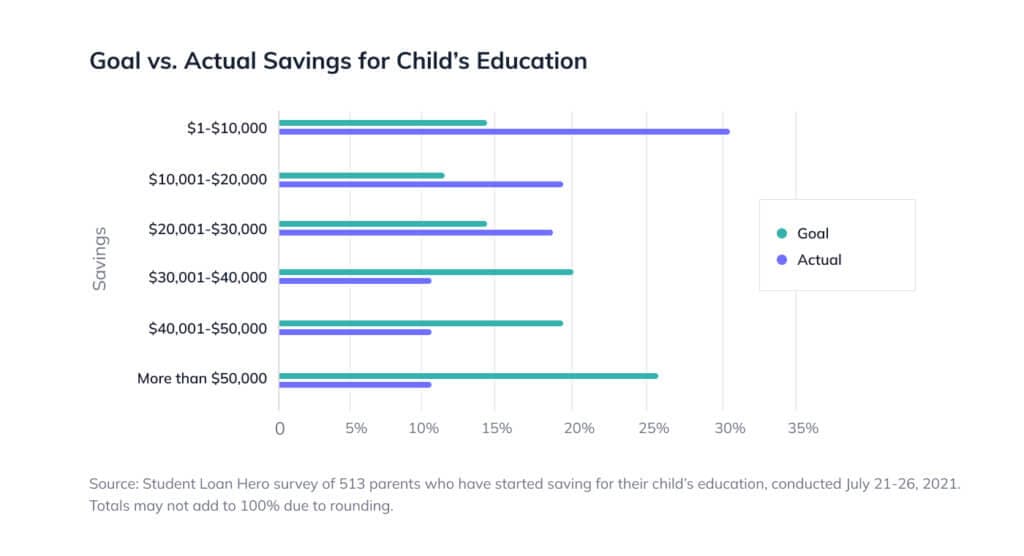

A recent study found that many of those who do save don’t reach their goals – especially those who aimed to have $30,000 or more stashed away for higher education.

If at all possible, you should avoid making a 401K withdrawal for education or using a 401k to pay for student loans. Not only will you pay extra taxes if you withdraw before age 59 ½, but you’ll also face a 10% penalty. Most importantly, it will chip away at the funds you’ve worked to save for your future.

Fortunately, there are solutions for paying for your child’s education that don’t involve drawing from your hard-earned retirement savings — or even taking out a loan. We explain some of the most common ones below, so you can determine the best way forward for your family.

529 Plans

A 529 plan is an investment account that’s specifically designated for education savings and provides tax benefits for those in certain states. There are two different 529 plans. Prepaid tuition plans let the account holder buy units or credits at select colleges or universities (usually in-state or public schools) for tuition only, though there are more than 250 private colleges which offer a plan through the Private College 529 Plan. The second kind of 529 plan is an education savings plan, which provides a bit more flexibility by allowing the borrower to put away money for tuition, fees, and room and board. Both of these plan types work very similarly to a Roth IRA, which we’ll discuss below.

IRAs

You may not have known that you can use an IRA withdrawal for college funding, but it’s possible if you keep certain restrictions in mind.

When it comes to IRA distributions for education, whether you’re pulling from a Roth IRA or traditional IRA matters. Since a Roth IRA is funded by post-tax dollars and a traditional IRA is funded by pretax dollars, you can take out the full amount of contributions from your Roth IRA without any penalties or fees (but not earnings).

In order to bypass the standard 10% early withdrawal penalty that is attached to a traditional IRA, you must provide proof to the IRS that the student you’re paying for is currently attending an eligible institution; you can’t use the funds after graduation to pay off loans. It’s also important to note that the amount of the withdrawal cannot exceed the qualifying expenses you’re seeking.

Student Loans

Of course, there are traditional student loans, including federal loans, private loans, and refinance loans. Federal loans, which are generally the easiest to qualify for and available to nearly every high school graduate, consist of direct subsidized loans, direct unsubsidized loans, PLUS loans (which we’ll explain a specific type of below), and direct consolidation loans. Private loans are typically more difficult to obtain due to credit requirements and come with more restrictions, so they’re often a second choice behind federal loans. Finally, a refinance loan can be used after a student graduates to replace an existing loan and secure a lower interest rate.

Parent PLUS Loans

These loans are federal student loans issued directly to parents and they’re intended to supplement school, state, or federal financial aid. To be eligible for one of these loans, you must be the biological or adoptive parent of a dependent undergraduate student enrolled at least half of the year. The maximum amount you can borrow is dependent on the school, as you can typically qualify for coverage of the total cost of attendance provided that you meet some minimum credit criteria and the student meets financial aid requirements.

Home Equity Options

If you’re a homeowner, you might also have the ability to access your home equity to cover your child’s college expenses. There are traditional home equity loans, which have the reliability of a fixed interest rate and predictable monthly payments. However, they involve taking out another loan on your home, which may be less than ideal depending on your specific situation.

You might also consider a home equity line of credit (HELOC), which provides flexibility in terms of access to cash and how frequently you can borrow. However, its variable interest rate means that your monthly payments will be unpredictable, and the lender can freeze the HELOC at any time in the case of a drop in home value or credit score.

Finally, a home equity investment can give you cash you need to partially or completely fund your child’s college tuition without the stress of another monthly payment. You receive cash in exchange for a share of your home’s future value and have 10 years to put it toward whatever you’d like.

As with any financial decision, weigh the long-term costs of each of them carefully. The total interest costs of student loans compared to solutions that involve your home equity may still end up being the more affordable option.

Tap into your equity with no monthly payments. See if you prequalify for a Hometap investment in less than 30 seconds.

You should know

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

More in “Financial goals”

The Sandwich Generation's Guide to Using Home Equity: Supporting Kids and Aging Parents

Can You Afford Your Mortgage on a Single Income? A Guide for Life's Transitions