Denver Homeowners Say Mortgages Make Other Financial Goals Tough

What’s making Denver feel house rich, cash poor? Colorado has one of the highest income-to-mortgage payment ratios at 15.54 percent, with an average monthly mortgage payment of $1,160. Denver, however, has wildly drastic price variations from neighborhood to neighborhood, and while values have increased 1.5 percent this year, Zillow predicts we’ll see a 0.5 percent decrease within the next year.

With equity built up in their homes but little to no cash on hand for more immediate expenses, 78 percent of Denver-area homeowners feel house rich and cash poor, and 22 percent of those homeowners feel this way most or all of the time.

Why Is This Happening?

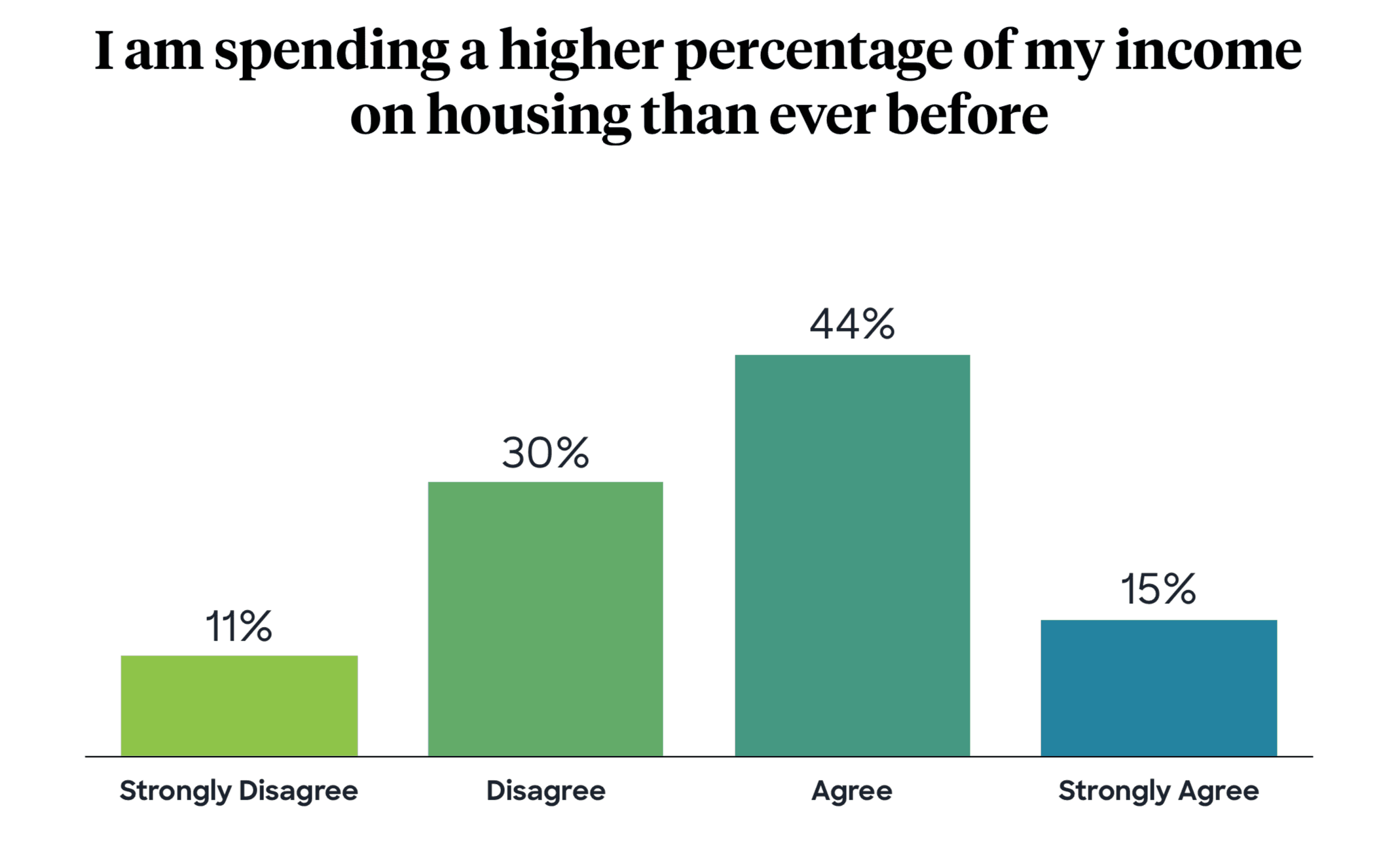

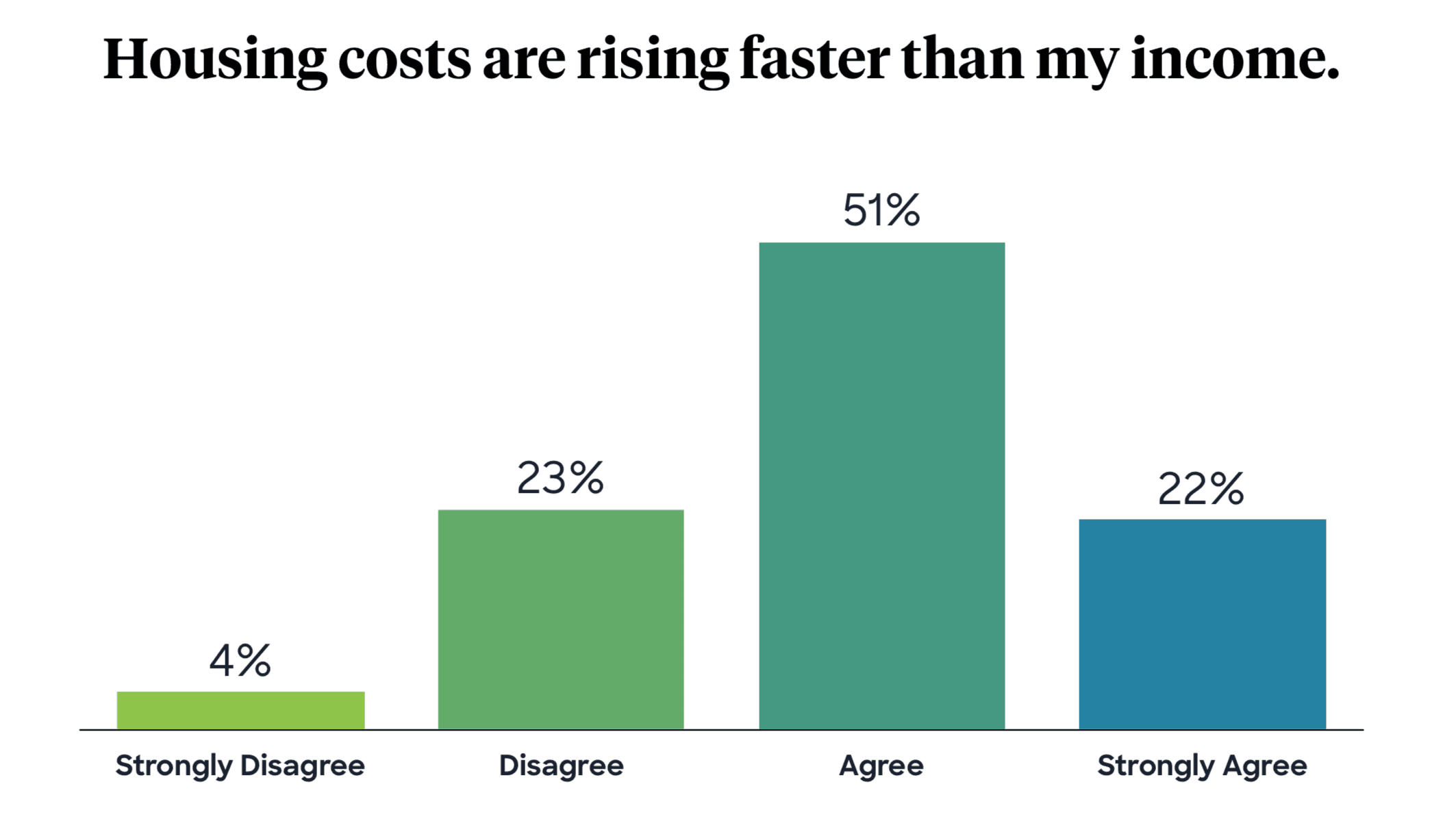

Since its infancy, Hometap has been studying the house-rich, cash-poor phenomenon that has been building since the Great Recession. The widening gap between wages and housing costs as well as the lack of attractive options to access home equity is largely to blame for this crisis. In fact, according to a recent Hometap study, 59 percent of Denver-area homeowners report their housing costs are rising faster than their income while 82 percent say they’re spending a higher percentage of their income on housing than ever before.

Why Does It Matter?

Our study of nearly 700 homeowners aimed to track the impact the house-rich, cash-poor crisis is having on homeowners across the country. What we found when we took a closer look at Denver was that it has the greatest contrast to national responses from the survey. For example, they’re the largest cohort to believe they’re building equity in their homes, and are on the lowest end of homeowners that don’t think they have any good options for turning their equity into cash.

Despite a rather optimistic outlook, Denver is seeing a slow-down on the job front, ranking 32nd for job growth out of 51 metros with a population of one million or more. As such, 78 percent of those surveyed fell between moderately to extremely stressed when it comes to the security of future income.

Home maintenance is another significant source of stress across all age groups and geographies surveyed, and that remains true for Denver. Eighty-two percent of Denver-area homeowners answered that they’re moderately to extremely stressed about the anticipated costs of home maintenance, and nearly half aired on the side of very to extremely stressed

The best way to prepare for costly emergency repairs is to set aside money each year—and keep it there even if you don’t end up using it. HGTV recommends saving 1–3% of your home’s value every year for home maintenance and repairs. Saving now can save you stress later.

See the national results of Hometap’s Homeowner Study

Access Your Equity, Eliminate Stress

If you’re like most homeowners, you have other financial goals you want to meet besides homeownership. But 52 percent of Denver-area homeowners agree high housing costs make it difficult to achieve other financial goals, whether that’s paying off debt, starting a business, or any number of goals.

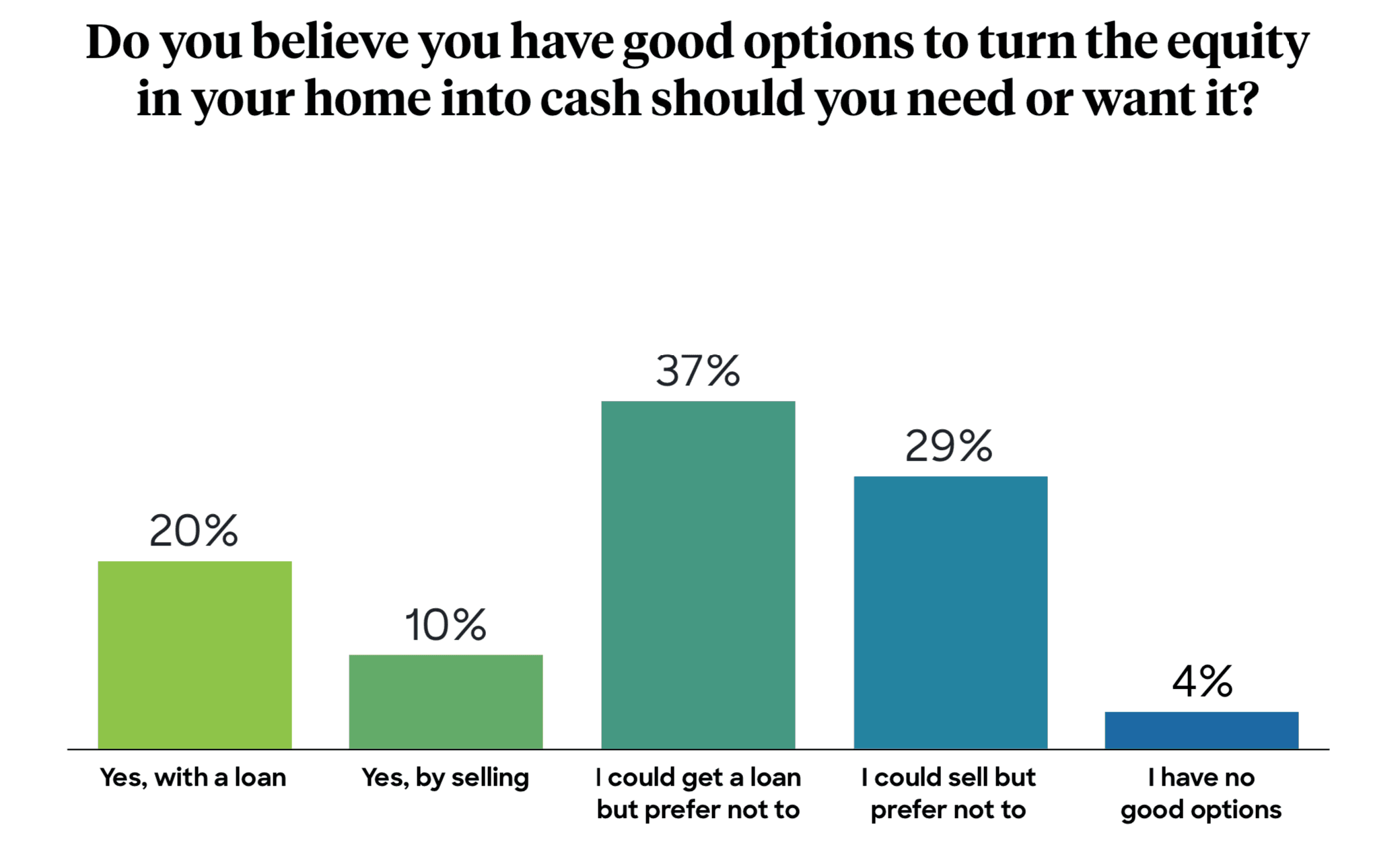

Homeowners may have difficulty achieving financial goals because they can’t access their home equity. In fact, 70 percent of

Denver homeowners in our study don’t feel like they have good options for turning the equity in their home into cash. Thirty-seven percent don’t want to take on a loan and the debt, interest, and monthly payments that come with it. Another 29 percent say they could sell their home to access equity but would prefer not to.

As a homeowner, you do have options. You can access home equity via a home equity loan, home equity line of credit (HELOC), cash-out refinance, or home equity investment—and not all of these options involve taking on additional debt.

The more you know about your home equity, the better decisions you can make about what to do with it. Do you know how much equity you have in your home? The Home Equity Dashboard makes it easy to find out.

You should know

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.